Welcome to another exciting blog of wikilifestyles.com

Introduction: Why do People Stay Poor

Are you tired of always living paycheck to paycheck? Do you wonder why you’re never able to save money or get ahead financially? Well, my friend, you might be stuck in the poverty cycle. Don’t worry, though, as in this blog post, we’ll discuss the six reasons why you’re always stuck in poverty, with some humor thrown in to lighten the mood.

1. You’re Stuck in a Debt Trap

Debt is the biggest hindrance to financial stability. If you’re constantly paying off debts, you’ll never have enough money to save for a rainy day or invest in your future. As the famous American investor, Warren Buffet, once said, “If you buy things you don’t need, you’ll soon be selling things you do need.”

Unfortunately, you don’t understand that, take for example a brand new car, you will be ravished by the EMI shown on the board, which is shown as just per lakh, while your existing car might be just 2 years old, and the vehicle dealership will get you the brand new car by exchanging your old car in a blink of an eye, and you won’t bother how much exchange value you got for that old car, it might be in a scrap value, with some so-called bonuses like exchange bonus, corporate bonus, etc., but if you calculate with a clear mind you can identify that deal is a total loss, which will extend the debt trap for some more period. same as in the case of other gadgets especially purchasing using your credit card

So, the next time you’re tempted to take out a loan for a new car or max out your credit card on the latest gadget, remember that debt is a trap that will keep you stuck in poverty. and also remember these banks, NBFCs, and vehicle dealerships are not here to serve you ultimately, they are here to do business on a monthly, daily, and hourly target basis

How Credit Card will make you in a Debt Trap

Credit cards have become an essential part of our financial lives, but they can also be a trap that leads to significant debt. Using credit cards can be tempting, especially when they offer various benefits and rewards, but overspending and high-interest rates can quickly add up, leading to a debt trap.

One of the most common ways credit cards can lead to debt is by encouraging overspending. It’s easy to swipe a card without thinking about the consequences, but every time you make a purchase with your credit card, you’re essentially borrowing money that you’ll have to pay back with interest which is huge. As a result, you may end up spending more than you can afford to repay, which can lead to a snowball effect of debt.

Credit cards also come with high-interest rates, which can make it difficult to pay off your balance if you’re only making the minimum payment. The longer it takes to pay off your balance, the more interest you’ll accumulate, and the more you’ll end up paying in the long run. This can keep you trapped in a cycle of debt that’s hard to break out of.

In addition to high-interest rates, credit cards often have hidden fees, such as annual fees, late payment fees, and balance transfer fees, which can make it even more challenging to pay off your balance and get out of debt.

Using credit cards irresponsibly can lead to significant financial losses, and falling into a debt trap is one of the easiest ways to do so. It’s essential to use credit cards wisely, avoid overspending, and pay off your balance in full each month to prevent falling into a debt trap.

In conclusion, credit cards can be a useful financial tool, but they can also lead to significant debt if used irresponsibly. Be aware of the potential pitfalls of credit card usage, and make sure to use them wisely to avoid falling into a debt trap.

2. You Haven’t Learned About Personal Finance

The basics of personal finance I learned from my grandma, handling the family budget, and keeping a small savings account in various areas, including a portion in the rice bowl and another portion in the wardrobe where the clothing is stored. I’m not sure where she got this knowledge; to the best of my understanding, she hasn’t even completed a metric pass.

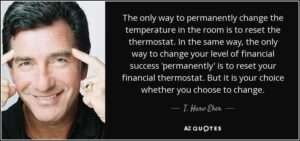

Personal finance is not taught in schools, we have to learn by ourselves about personal finance, such as budgeting, saving, and investing, which is essential if you want to break the poverty cycle. As the businessman and motivational speaker Harv Eker, once said, “The only way to permanently change the temperature in the room is to reset the thermostat. In the same way, the only way to change your level of financial success ‘permanently’ is to reset your financial thermostat, but its your choice to change”

Personal Loan Makes you a Glorified Beggar

While personal loans can be a useful tool to help with unexpected expenses or other financial needs, they can also lead to a cycle of debt that can leave you feeling like a glorified beggar.

One of the main problems with personal loans is that they often come with high-interest rates, which can quickly add up if you’re unable to pay off your balance quickly. This can lead to a situation where you’re constantly paying off interest, but never actually making progress on paying off the principal amount, which can make you feel like you’re begging for money.

Additionally, taking out a personal loan can also damage your credit score, which can make it harder to secure other loans or credit in the future. If you’re unable to pay off your personal loan on time, you could end up defaulting on the loan, which can result in collection calls and other stressful situations that can make you feel like you’re begging for mercy.

Ultimately, the key to avoiding feeling like a glorified beggar when taking out a personal loan is to use them responsibly. Make sure you have a plan for paying off the loan, and only take out what you can afford to pay back. As Dave Ramsey once said, “Debt is dumb. Cash is king.” By avoiding unnecessary debt and using personal loans wisely, you can avoid feeling like a glorified beggar and achieve your financial goals.

3. You Lack an Emergency Fund

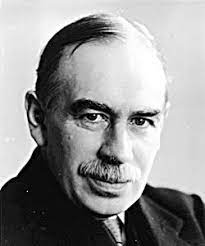

Life is unpredictable, and emergencies can happen anytime, anywhere. If you don’t have an emergency fund, you’ll have to rely on credit cards or loans to cover unexpected expenses, which can lead to more debt. As the British economist, John Maynard Keynes, once said, “The importance of money flows from it being a link between the present and the future.” Therefore, it’s essential to have an emergency fund that can cover at least three to six months’ worth of living expenses.

4. You Don’t Have a Money Plan

A money plan is like a roadmap for your finances. It helps you set financial goals and create a plan to achieve them. Without a money plan, you’re just drifting through life, hoping that things will work out. Once again i am quoting the words of Dave Ramsey, “A budget is telling your money where to go instead of wondering where it went.”

5. You’re Investing in Unwanted Stuff

Investing in material possessions, such as a fancy car or a luxurious house, might make you feel good in the short term, but it won’t bring you long-term financial stability.

Consider Virat Kohli, the former captain of the Indian cricket team, who admitted to selling the majority of his vehicle collection, labeling them “impulsive purchases” Virat Kohli said that he sold most of the cars he bought over the years, referring to them as “impulsive buys.” he can buy them because he is way richer and it is an all-cash purchase, but everyone can’t be like him, but the problem arises if you imitate those celebrities by taking out a loan to purchase them.

How Impulsive Purchase will make you in a debt trap

You’re out shopping and see something you’re just fascinated. Maybe it’s a new outfit, a piece of jewelry, or a fancy gadget. You’re convinced that you can’t live without it, so you make an impulsive purchase. While it may feel great at the moment, impulsive purchases can quickly lead to a debt trap that’s hard to escape. E-commerce platforms are the main trap for impulsive purchases nowadays, as they ravish us with lots of nonsense offers and facilities like cash on delivery,

The problem with impulsive purchases is that they’re often made without any thought to the consequences. You may not have the money to pay for the item, so you put it on a credit card or take out a loan. Over time, these small purchases can add up, leaving you with a significant amount of debt that’s hard to pay off.

Again i am quoting Warren Buffett’s’ same words, “If you buy things you don’t need, soon you will have to sell things you need.” Impulsive purchases can quickly become a vicious cycle of buying things you don’t need, racking up debt, and then having to sell things you actually do need just to make ends meet.

One way to avoid falling into the trap of impulsive purchases is to create a budget and stick to it. Make a list of the things you need and prioritize your spending accordingly. If you do find yourself wanting to make an impulsive purchase, take a step back and think about it for a few days. If you still want it after a few days, then consider making the purchase.

To avoid impulsive purchases is to focus on experiences rather than things. Instead of buying new stuff, consider taking a trip, trying a new hobby, or spending time with loved ones ,or else start writing blogs as I am doing ,by focusing on experiences rather than material possessions, you may find that you need less than you think.

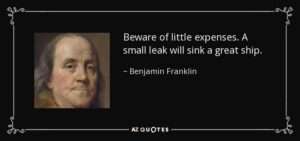

Impulsive purchases may feel great at the moment, but they can quickly lead to a debt trap that’s hard to escape. By creating a budget, focusing on experiences rather than things, and taking a step back before making a purchase, you can avoid falling into the trap of impulsive purchases and achieve your financial goals. As Benjamin Franklin once said, “Beware of little expenses; a small leak will sink a great ship.”

6. You’re Trying to Get Rich Quick

If you’re always looking for a quick fix to your financial problems, you’ll likely fall prey to scams and schemes that promise to make you rich overnight.

Nowadays it’s easy to fall into those traps, as some of the gamblings are legalized, one such kind is Online Rummy, which has been banned in some states in India, another misconception is that whether these gamblings are skill-based or luck based, just one thing you should understand those companies conducting this so-called legalized business are not here to make you rich, they are all big corporates they are throwing money to promote the business, which they will make sure their part of the share will get back with profit, I believe you know well who sponsored 2020 IPL in India,

Remember, building wealth takes time and effort. As the American businessman and philanthropist, Andrew Carnegie, once said, “The way to become rich is to put all your eggs in one basket and then watch that basket.”

Conclusion: Why do People Stay Poor

Being stuck in poverty can be frustrating and overwhelming, but it’s not permanent. By recognizing the reasons why you’re stuck in poverty, such as being in a debt trap, lacking personal finance knowledge, not having an emergency fund, not having a money plan, investing in material possessions instead of yourself, and trying to get rich quick, you can take steps to break the cycle.

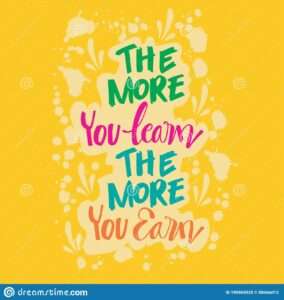

As Warren Buffet once said, “The more you learn, the more you earn.” So, take the time to learn about personal finance, create a budget, build an emergency fund, invest in yourself, and be patient. Remember, wealth-building takes time and effort, but perseverance and determination can break free from the poverty cycle and achieve financial stability.

FAQ:

1 Why do some common things which people stay poor?

People stay poor due to several factors such as lack of education, lack of job opportunities, low wages, inadequate access to financial services, and systemic inequalities.

2. How can people break out of poverty?

Breaking out of poverty requires a multi-faceted approach, including education and training, access to better job opportunities, financial education, and support from government and non-governmental organizations.

3. What are some common misconceptions about poverty?

One common misconception is that people living in poverty are lazy or don’t want to work. This is not true as many people in poverty work multiple jobs and still struggle to make ends meet.

4. How does poverty affect mental health?

Poverty can have a significant impact on mental health, leading to increased stress, anxiety, and depression. It can also result in a lack of access to mental health services and support.

5. Can financial literacy help break the poverty cycle?

Yes, financial literacy can play a significant role in breaking the poverty cycle. It can help individuals understand how to manage their finances, avoid debt traps, and build wealth over time.

6. How does systemic inequality contribute to poverty?

Systemic inequality, such as discrimination based on race or gender, can limit access to education, job opportunities, and financial services, leading to a cycle of poverty that is difficult to break.

7. How can communities support those living in poverty?

Communities can support those living in poverty by providing access to basic needs such as food and shelter, offering job training and education, and advocating for policies that promote economic equality.

8. What are some ways individuals can make a difference in reducing poverty?

Individuals can make a difference in reducing poverty by volunteering with organizations that provide support to those in need, advocating for policies that address poverty, and supporting local businesses and communities.

9. How can government policies help reduce poverty?

Government policies such as increasing the minimum wage, providing access to healthcare and education, and implementing social safety nets can help reduce poverty and provide support to those in need.

10. Is poverty a solvable issue?

While poverty is a complex issue, it is solvable through a combination of government policies, community support, and individual action. By working together, we can create a world where everyone has access to the resources and opportunities they need to thrive.

Good post. I learn something new and challenging on blogs I stumbleupon on a daily basis. Its always exciting to read content from other authors and use a little something from other web sites.